Quoted: “Masters went on to say that, because financial services involve Americans’ livelihoods (and not just, say, their taxi ride to Brooklyn), regulations ruling the space are many multitudes more complex than they are in other industries — and the 100-plus year-old banks have a leg up in dealing with these rules.

“Anyone who imagines that as a result of the advent of new technology we will see a world where incumbent financial institutions who provide vital, heavily-regulated intermediated services, custodial services, safe-keeping services will be decimated and completely removed from the picture overnight is just naive and wrong,” she said, pointing out that customers of legacy banks can pay bills and deposit checks through their iPhones — so it’s not as if there’s been no innovation in traditional financial services.”

Read the article here > http://www.forbes.com/sites/maggiemcgrath/2015/10/20/will-fintech-upstarts-do-to-banks-what-uber-has-done-to-taxis-or-will-the-banks-ultimately-win/

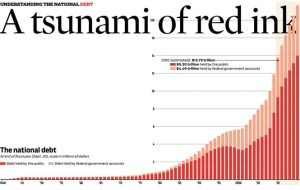

At the end of 2015, the US national debt will be 18.6 trillion dollars. With such a big number, it’s tempting to put it in perspective by comparing it with things more easily envisioned. Alas, I can not think of anything that puts such an oppressive and unfair burden into perspective, except to this:

US debt represents a personal obligation of $60,000 for each American citizen. And it is rising quickly. Most of our GDP is used simply to pay down interest on that debt. Few pundits see a way out of this hole.

In my opinion, that hole was facilitated in August 1971, when the US modified the Bretton Woods Agreement and unilaterally terminated convertibility of the US dollar to gold. By forcibly swapping every dollar in every pocket and bank account with the promise of transient legislators, individual wealth was suddenly based on fiat instead of something tangible or intrinsic.

Feds Meet: No interest rate hike

The benchmark interest rate set by the US Federal Reserve Board is currently between 0 and 0.25%. It has been at or near zero since 2006.

By now, Lifeboat readers know that 20 hours ago, the US Federal Reserve board decided to not hike the benchmark interest rate. The Fed did, however, signal that they still intend to raise interest rates at a future meeting—perhaps in October or December.

The announcement came just after US equity markets closed. But, in what has become a most odd news coverage of a non-event, the immediate reaction was to lift the Asian stock markets, which were still open during the announcement.

I am a frequent contributor to Quora. I field many questions on economics, politics, law, and even physics. You might be inclined to check out my credentials as pundit of macro-economics. Don’t bother…There are none! I am an armchair economist (this is the same as saying: “I am not an economist”). But I certainly follow these things closely, and have an informed opinion.

Today, I was asked this: What would happen if the fed had raised interest rates?

The question asked specifically about the effect on other interest rates, but a more interesting exercise might be to speculate on the state of the economy. Here then, is a comon-sense response…

If we could freeze all other conditions and avoid the effects of public confidence, likely change in debt, debt rating, etc… If we ignore these things, then the direct result of raising the interest rate for a given national currency is to attract outside money. That is, we would see an increase in foreign conversion into dollars and a movement of US assets from stocks and bonds into currency or currency equivalents. This is a simple result of the higher payout that one would expect after a raise in interest rates.

In theory, the sift of international assets and investment into dollars does four things:

It strengthens the value of the dollar, thereby increasing the take-home potential of US workers and the number of things US residence buy from overseas (because a slightly higher fraction of organizations seek dollars)

It increases income for anyone tied to published interest rates, such as many senior citizens.

It increases interest payments from anyone tied to published interest rates. For anyone deeply in debt on instruments such as credit cards or home equity, this can have a devastating impact—causing minimum payments to rise by many times the interest rate hike.

It increases US national debt, because so much of the economy is built on forward loans in the form of Treasury notes. With an interest rate increase, the US must pay more on both new debt and the financing of massive outstanding debts.

This is all theoretical, of course. In practice, one of the first effects is for individuals and institutions to wonder: “How can the US possibly pay out on debt at an increased rate?”. [possible answer]*

One very obvious effect is that many individuals will further lose confidence in the American economy or the will of American’s to honor the national debt. Because of this, the effect of raising the interest rate (for the first time in 9 years) is not easy to predict. Despite massive uptake on US debt, the Chinese and energy producing nations have limits to what they can believe. A subtle switch in their investment activity (or the determination to move away from a dollar-based reserve) will have massive repercussions, especially for the US.

_____________ * Some pundits argue that US debt and payments can continue to grow, because the ability to accommodate these things are protected by these things:

a recovering economy

increased activity from the new investors

need for producer nations to seize on a massive consumer market

need for producer nations to invest their gains

But, a growing number of economists, investors, analysts, credit bureaus, and citizens don’t buy this argument! They point out that it kicks-the-can down the road and foists untenable debt on future generations. They would prefer that the US reign in spending and pay down debt.

In this regard, being the world’s reserve currency has helped hook the US on debt, and it has ballooned out of control. Transitioning to a firmly capped currency that is not controlled by legislation or a reserve board would help the country avoid massive debts (those that exceed the willingness of bond holders to finance) and to do what it must do.

In my take, the real question is not “What if the Fed has raised interest rates?” The real question is:

Does the U.S. have the courage to link its currency to something durable — and beyond control of transient political winds and a debt pyramid?”

Sure, we must still honor the excess of the past 40 years. But with gold, or Bitcoin, at least we will have solid underpinnings and incentives to spend within our means.

This short post is not about Bitcoin. It’s about a new method of organizing and arbitrating communications that is at the heart of Bitcoin

We hear a lot about the blockchain. We also hear a lot of misconceptions about its purpose and benefits. Some have said that it represents a threat to banks or to governments. Nonsense! It is time to form a simple, non-political, and non-economic explanation…

What is a Blockchain?

The blockchain is a distributed approach to bookkeeping. It offers an empowering, efficient and trusted way for disparate parties to reach consensus. It is “empowering”, because conclusions built on a blockchain can be constructed in a way that is inherently fair, transparent, and resistant to manipulation.

This is why blockchain-backed systems are generating excitement. Implemented as distributed and permissionless, they take uncertainty out of accounting, voting, legislation or research, and replace it with trust and security. Benefits are bestowed without the need for central authority or arbitration. The blockchain not only solves a fundamental transaction challenge, it addresses communication and arbitration problems that have bedeviled thinkers since the ancient Egyptians.

For most of us, figuring out the value of something that we want, comes from research. If you want a new set of wine glasses, you check the price online. Perhaps you consult a catalog. If the set of 8 stemware goblets that you like are a current model from a major company, there are probably many places to buy them. If there are multiple Ebay sellers and many recently completed sales, then you can establish the value with precision.

I’ve written a lot of Bitcoin articles on this Lifeboat Blog and elsewhere, so, let’s dig a bit deeper this time. Let’s talk about from where value really comes.

Supply and Demand

In the end, an item’s value is a direct result of supply and demand. It’s no different with a currency. And let’s be clear: Despite a raging debate, Bitcoin is a currency and not just a payment instrument. How can I be certain? Try this mental exercise—

Western Union money orders and Amazon Gift cards are each trusted monetary instruments. They facilitate cash transactions. But are they currencies with inherent value? If so, there would be no need to denominate them in units of fiat currency.

A money order is only worth something before it is redeemed. The gift card is only worth $500 when it is purchased or received as a gift. As the $500 is depleted, it becomes worthless. Eventually, it is just a piece of plastic. But like a dollar bill, a bitcoin can be circulated over and over. You may believe that its value comes from the government, but more realistically, its value arises from brand recognition and from pure supply and demand—not from a trusted redemption authority.

Bitcoin isn’t the first ethereal stash of bits with value. But it is more durable than others. The latest Pixar film on DVD or On Demand from your cable service provider has value. But piracy reduces the value dramatically. The supply is no longer scarce (no matter the demand) because of the ease and willingness to replicate digital files in any quantity. A Picasso painting is very rare, but it is so scarce, that we cannot gather enough data points to establish a stable value. Even worse, it’s not portable, divisible or fungible and it is nearly impossible to validate in the hands of the average person.

But, commodities like iPhones, Doritos tortilla chips—or even non-branded things, like Idaho potatoes, have a large and fluid market. These things have very measurable value and we can track the change in value over time.

People like to think that money is different than other commodities. In practice, it differs only by its handling characteristics: Compared to a Picaso painting or a new iPhone 6, currency has these properties. It is:

portable

fungible

divisible

widely recognized

resistant to forgery

backed by something tangible

Bitcoin has all of these characteristics. In fact, it surpasses your national currency in every way. But many people are confused about that last niggling detail… Aristotle called it “intrinsic value”. They worry that there is no gold—or at least the promise of a stable government—to establish and stand behind the value of a bitcoin unit (BTC). The concern is understandable, but it is wrong.

Recall that value arises through supply and demand and not simply because of authority or promises. The real question is “Can we trust that the supply is limited and that the demand is durable?”. That is, will my coin be recognized, coveted and honored in the future?

The Case Against Bitcoin as a Currency

Here are some frightening facts (frightening for some cryptocurrency enthusiasts and early adopters): Bitcoin is manufactured out of thin air. It lacks the underpinnings of a traditional currency. Referring to that last item on Arisotle’s list above, Bitcoin seems to fail the test of intrinsic value, because it lacks at least one of these properties:

A fractional reserve requirement

An edict to remit taxes in Bitcoin

A promise of a trusted authority

Any claim of pegging it to the value to some essential commodity (intrinsic value)

Bitcoin doesn’t even offer a perception of uniqueness. The formula is open for anyone to copy. You could create a competing ‘Bob-coin’ tomorrow.

In the absence of at least one of these things, detractors claim that Bitcoin lacks a foundation—and so it is effectively worthless. But value does not come only from authority. It comes from trust and is goverend by supply and demand.

The dollar is backed by trust — Not gold, math, nor even history

In fact, math may be a more trusted ‘authority’ than the directors of your national treasury and reserve board. Supply and demand leads to more tangible value than bankers, especially if the math leads you to believe that the demand will continue to outpace the supply. In fact, this is the primary reason that you are comfortable with a $20 bill in your pocket. You have a pretty good idea, that next week, it will still buy 2 movie tickets or 2 pizzas.

Bitcoin has achieved a “two-sided network effect” (Google the term and the economist “Marshall Van Alstyne”). It has captured the public imagination more than Picasso. It cannot be manufactured. With a reasonable understanding of wallets, it cannot be seized, stolen or lost.

The ability to mine new bitcoins is capped with a total supply of 21 million units, and so there is no opportunity for governments to inflate it through mismanagement of taxation or spending. They cannot even inflate it with good intent (for example, when they need to repair a bridge or provide for the poor). Instead, the ability to pay for these services (and all other government functions) forces them to live within a balanced budget. Spending cannot outpace the revenue generated by taxes and bonds. In a Bitcoin economy, the bonds will more likely be paid back by user fees rather than the future debt of unborn generations.* You get the point: Because governments no longer control the printing press, they cannot make hollow promises and then kick the problem into the next administration. With a limited money supply that everyone recognizes as money, governments are forced to live within their means.

What About Uniqueness?

The last item in the list above decries Bitcoin’s lack of uniqueness. You cannot mint your own bitcoins of course—but you can create an equivalent bitcoin ecosystem yourself. If your name is Bob, you can call it Bobcoin. Many countries and organizations are already doing this.

This is really no different than the US Dollar or your own national currency. The government note is difficult to counterfeit, but so is your own signature when placed on a fancy printed currency (Let’s call it a Bob-Buck). The problem is that the dollar is widely recognized, trusted and accepted, but few people other than your kids are collecting Bob Bucks.

You would face the challenge of spurring adoption. Whether it’s Bob Bucks (paper) or Bobcoin (cryptocurrency), how will you get the world to covet, mine and trade your new currency? That’s the point of a two-sided network. It becomes increasingly more difficult after one method rises to the top—especially if that method is open, transparent and extensible. Bitcoin is open. It is subject to worldwide scrutiny. But this works both ways. Bitcoin can also add incremental improvements that are part of any pretender to the throne.

Bitcoin is not just a transient coin-du-jour. It evolves and so it will not die.

How Can the Value be Measured?

I get this question a lot, and so I am adding the answer here. There is no need to measure the value of Bitcoin or define debt. Its value floats with supply and demand like a true world currency. Because the supply growth is capped and well understood, it is resistant to manipulation. As time goes by, it becomes far less likely to exhibit wild swings in value.

A few years from now, if Bitcoin spikes or tanks by 10% in a short time, you will be more likely to wonder “What is affecting the dollar?” (or Euro), rather than “What is affecting Bitcoin”. Consumers will budget for the cost of a new car or refrigerator in BTC rather than dollars or Euros. You will even see catalogs that print prices in BTC and honor them for the life of the catalog or online sale. After all, in an international market, it makes sense to quote a price in units with no geopolitical boundaries, just as we quote time in UTC (formerly called GMT).

Are these predictions crazy? They are not even bold. For us, here at Lifeboat Foundation, they are rather obvious. If we can be accused of dreaming, it is because we are ahead of the game. Look ahead, yourself. The signs are clear…

If Bitcoin has Value, What is the Value?

As Bitcoin adoption moves past enthusiasts and early adopters, the capped supply of coins (21 million, max) will be spread thinner and thinner. This doesn’t play out like a classic shortage, because unlike a supply squeeze on food or medicine, you can work with a smaller piece of the pie each year. The piece needed to pay for a car or an iPhone simply gets smaller as the unit price floats higher and higher.

Last year, I set up an equation to predict how high Bitcoin will float in 5 or 10 years. It involved a lot of WAGs (wild *ss guesses). Although I am a pundit, I am not a mathematician, and so the attempt was incomplete. No need to rehash that exercise.

As Hysteria Withers, Bold Becomes Mundane

Eventually consumers, banks, brokers, and governments will recognize that Bitcoin is a far greater opportunity than it is a threat. It pulls the world together by decoupling currency controls from national agenda, inflation, manipulation and loss (You can back up your Bitcoin. Try doing that with your paper money or a defunct bank).

Philip Raymond is CEO and Co-Chair of CRYPSA, The Cryptocurrency Standards Association.

_____________ * This is just one reason why an eventual transition to Bitcoin (as currency, and not just as a payment instrument) is in the national interest. It demonstrates to citizens that monetary policy is backed by more than growing debt, inflation or the promises of transient officials. It returns any government or economic entity to a non-inflationary, limited-supply pie. The pieces of pie can grow in value, but the pie cannot be watered down by printing more ingredients, counterfeit or even by enemy action.

Peter Thiel’s Valar Ventures and Citigroup’s Citi Ventures have backed a New York-based startup that lets retail investors place orders for securities on news websites, financial blogs and mobile apps, as investments in young financial-technology companies continue to grow.

Last year, Google began experimenting with hardware-based schemes for user-authentication, while Apple added two factor authentication to iCloud and Apple ID users. They began sending a verification code to users via a mobile number registered in advance.

Security pundits know that two factor authentication is more secure than simple passwords. As a refresher, “Factors” are typically described like this:

Something that you know (a password — or even better, a formula)

Something that you have (Secure ID token or code sent to cell phone)

Something that you are (a biometric: fingerprint, voice, face, etc.)

The Google project may be just another method of factor #2. In fact, because it is small (easily misplaced or stolen), it simplifies but does not improve on security. I suggest a radical and reliable method of authentication. It’s not new and it’s not my idea…

Back in 1999, Hugh Davies (no relation to Ellery) was awarded a patent on a novel form of access and authentication. It capitalizes on the human ability to quickly pick a familiar face out of a crowd. Just as with passwords, it uses something that you know to log in, purchase, or access a secure service. But unlike passwords, the “combination” changes with every use, and yet the user needn’t learn anything new.

Hoping to commercialize the technique, Davies joined another Brit, Paul Barrett, and formed Passfaces (originally, Real User Corporation). Incidentally, it is quite difficult to research Passfaces and its history. Web searches for “face recognition”, “access”, “authentication” and “patent” yield results for a more recent development in which a smart phone recognizes the face of authorized users, rather than users recognizing familiar faces. (Google, Samsung and Apple are all beginning to use face recognition on mobile devices). In fact, the Passfaces method is quicker, uses less resources and is far more reliable.

I have long been disappointed and surprised that the technique has never caught on. It is a terrific method with few drawbacks. Used alone, it is better than other methods of 1 or 2 factor authentication. Add a second factor and it is remarkably secure and robust.

How it Works:

When accessing or authenticating (for example, logging into a corporate VPN or completing a credit card purchase), you are presented with a tiled screen of individual faces. I prefer a big 15×5 grid = 75 images, but Passfaces uses sequential screens of just 9 faces arranged like the number pad on an ATM.

Just click on a few familiar faces. That’s all! Oddly, Passfaces discourages the use of known faces. Their research, with which I respectfully disagree, suggests that users should train themselves to recognize a few faces from the company’s stock library. In my preferred embodiment, users upload a dozen photos of people they know at a glance—preferably, people that they knew in the past: A 3rd grade music teacher, a childhood friend who moved away, the face on an oil painting that hung in the basement until Dad tossed it in the fireplace. Now, add the boss who fired you from your first job, the prom queen who dumped you for a football jock, and that very odd doorman who stood in front of a hotel in your neighborhood for 20 years. Photos of various quality and resolution, but all scaled to fit the grid. Some are black & white, perhaps scanned from an old yearbook.

Using my preferred example of 75 faces, suppose that 5 or 6 of the images are from your personal shoe box of old photos. The rest are randomly inserted from all over the internet. How long would take you to click on 3 of the 5 or 6 familiar faces in front of you? (Remember: They are old acquaintances. Even a spouse would have difficulty picking out 3 faces from your early life—as they looked back then). Surprise! You will click them instantly, especially on a touch screen. You won’t need even a second to study the collage. They jump off the screen because your brain perceives a familiar face very differently and faster than anything else.

Of course, the photo array is mixed in different ways for each authentication and it incorporates different friends from your original upload. In fact, if a user sees the same faces in the next few transactions, it is a red flag. Someone has spied on the process, perhaps with a local camera or screen logger. In legitimate use, the same faces are not recycled for many days and are never shown together on the same screen.

Facebook uses a variant of this technique when their servers sense your attempt to login from new equipment or from another part of the country. They show you individuals that you have friended, but that were uploaded and tagged by other users. If you cannot identify a few of your own friends, especially the ones with which you have frequent social contact, than it’s likely that your login attempt deserves more scrutiny.

I don’t know why Passfaces or something like it has failed to catch fire. Perhaps the inventor refuses to license the method at reasonable cost or perhaps he cannot find a visionary VC or angel consortium to more aggressively promote it. If I had invented and patented facial-array authentication, I would attempt to market the patent for a short time focusing on very large network companies like Microsoft, Google, Cisco or Akamai. If I could not license or sell the patent quickly, I would hesitate to go it alone. (I have tried that route too many times). Instead, I would place it in the public domain and profit by being the first, and most skilled practitioner at deployment. I would train and certify others and consult to organizations that use or commercialize the technology.

I used this approach in promoting my own patent which describes an economic barrier to spam (after failing to exploit the invention with my own company). Later, I started with this approach in my research on Blind Signaling and Response and on Reverse Distributed Data Clouds. I recognized that rapid adoption of transformative technology like facial grid authentication, can be thwarted by defensive IP practice.

« Branching somewhat off topic, a developmental biologist at Imperial College in London, has published a proof that Saira Mohan has the world’s most beautiful face, irrespective of the observer’s race. That’s Saira at left. Her mother is French/Irish and her father is Hindoo.

__________ Philip Raymond is Co-Chair of The Cryptocurrency Standards Association [crypsa.org] and chief editor at AWildDuck.com. He consults to cloud storage vendors in areas of security, pri– vacy & network architecture, but has no ties to Passfaces or the authentication community.

July 9 update: 3 days after posting, Visa acknowledged that Bitcoin has a future in payments. This is an understatement, of course. The bank described below goes a step further by acknowledging that the entire financial infrastructure may cave to cryptocurrencies.

French bank BNP Paribas warned customers and investors that the technology behind bitcoin might one day overtake conventional, account-based financial institutions, thus rendering existing companies redundant (that’s British for “obsolete”).* It’s a tectonic acknowledgement from one of the world’s biggest banks.

Analyst Johann Palychata writes in the company’s magazine Quintessence that Bitcoin’s blockchain, the underlying architecture that allows cryptocurrency to function, “should be considered as an invention like the steam or combustion engine,” that has the potential to transform the world of finance and beyond.

Check out the full story by Oscar Williams-Grut at Business Insider.

* Although Bitcoin will obsolete the current service mix of financial institutions, it is my opinion that for savvy governments and established businesses, it represents a long term opportunity rather than a threat. —PR

__________ Philip Raymond is Co-Chair of The Cryptocurrency Standards Association [crypsa.org] and chief editor at AWildDuck.com

Sure—You know the history. As it spread from the geeky crypto community, Bitcoin sparked investor frenzy. Its “value” was driven by the confidence of early adopters that they hitched a ride on an early train, rather than commercial adoption. But, just like those zealous investors, you realize that it may ultimately reduce the costs of online commerce, if and when if it becomes widely accepted.

But what is Bitcoin, really? To what class of instruments does it belong?

• Ardent detractors see a sham: A pyramid scheme with no durable value; a house of cards waiting to tumble. This is the position of J.D, an IRS auditor who consults to The Cryptocurrency Standards Association. As devil’s advocate, he keeps us grounded.

• This week, MasterCard was only slightly less dour. They claim that the distributed nature of Bitcoin will ultimately cause it to unravel. They want us to believe in the necessity of a trusted authority as broker/guarantor/arbiter. I get it! After all, the block chain is a serious threat to the legacy model for moving money

• Many people recognize that it can be a useful transaction medium—similar to a prepaid gift card, but with a few added kicks: Decentralized, low cost and private.

• Or is it an equity asset, traded by a community of speculative investors, and subject to bubble psychology? If so, do the wild swings in its exchange rate diminish its potential to be used as a payment mechanism?

• Full-fledged ehthusiasts say that Bitcoin has the potential to be a full-fledged currency with a “real value” that floats based on supply and demand. Can something that lacks intrinsic value or the backing of a bank or government replace national currency?

Regardless of your opinion about Bitcoin, it does one thing that few pundits dispute: Sure, the exchange value fluctuates—but for those who don’t plan to retain holdings as an asset, it reduces transaction costs to —nearly zero. This characteristic, alone, is a dramatic breakthrough.

Peering Into the Future?

Removing friction is certainly what it is all about. As a transaction medium, Bitcoin achieves this, but so does any debit instrument, or any account in which a buyer has retained house “credit”.

Currently, there is a high bar to get money exchanged into and out of Bitcoin. It’s a mess: costly, time consuming and a big hassle. Seriously! Have you tried using an exchange? Even the most trusted one (Coinbase of San Francisco) makes it incredibly difficult to get money in and out of BTC, prior to establishing your account, identity and banking history. Fortunately, this situation is gradually improving.

Where Bitcoin really shines (or more accurately, when it will shine), occurs at the time when more vendors choose to leave revenues in BTC, pending their own purchases from suppliers, shareholder payouts, or simply as retained savings.

When this happens, all sorts of good things will follow…

• A growing fraction of sellers leave their bitcoin in their wallets, realizing that they will need to spend it for their own labor and materials.

• Gradually, wild exchange-rate gyrations diminish—not because fewer people are exchanging money, but because the Bitcoin supply/demand value is driven more by actual commerce than it is by speculation.

• Sellers begin pricing merchandise in Bitcoin rather than national currencies—because they are less anxious to exchange out of BTC immediately after each sale.

When sellers begin letting a fraction of bitcoin revenues ride—and as they begin pricing goods and services in BTC—a phenomenon will follow. I call it the tipping point…

• If goods and services are priced in BTC, then everyone involved saves money and engages in transactions more efficiently.

• If goods and services are priced in BTC, then the public will begin to perceive exchange rate volatility as a changing dollar rather than a changing bitcoin.*

• If buyers also begin to save their BTC (i.e. they do not worry about immediately moving it back to national currency), it means that Bitcoin is being perceived as a stored value—not just an exchange chit. That may seem to be a subtle footnote, but the ramifications are earth shaking. That earthquake is the world gradually moving away from centralized treasury-issued bank notes and toward a unified and currency that we can all trust.

People, everywhere, will one day place their trust in a far more robust and trustworthy mechanism than paper promissory notes printed by regional governments. A brilliantly crafted mechanism that is fully distributed, p2p, transaction verified (yet private), has a capped supply and is secure.

What Then?

O.K. So we believe that Bitcoin is the future of money and not just a replacement for credit cards. But what does this really mean? Can the series of cause-and-effect be extrapolated beyond widespread user adoption? Absolutely! …

Adoption of Bitcoin as a stored value (that means as a currency) leads to the gradual realization among governments that Bitcoin is not a threat to sovereignty nor even to tax policy. Instead it presents unbounded opportunity: The opportunity to stabilize markets, eliminate inflation, reduce costs and restore public trust. In short, Bitcoin will ultimately level the playing field, revive entire economies, transform the role of government, and save consumers and businesses billions of dollars each year.

Did I mention that Bitcoin is the future of commerce and a very possible successor to legacy currencies? Aristotle must be smiling.

* We tend to think of the dollar as more ‘real’ than Bitcoin. It is not! It has only one advantage. At the end of the day, taxpayers must settle their debts in the currency demanded of their nation. But as Bitcoin adoption gains traction—even if only as a transmitting medium—fiat currencies will gradually become marginalized as play money. That’s because they are susceptible to inflation, politics and manipulation. Bitcoin is held to a higher standard. It is governed by pure math. Despite high-profile news of the day, Bitcoin will even become more resistant to loss and theft than dollars, once tools and practices become well established.

Uncle Sam can lease the US Treasury building to pay off debt brought about by inflation

Ric Edelman is one the top financial advisors in the US. His firm, Edelman Financial Services, has 41 offices across the country. And he thinks, all things constant, most financial advisors as we’ve known them won’t be around much longer.

At Exponential Finance, Edelman said, “I firmly believe that in the next ten years, half of all the financial advisors in this country will be gone.” Read more

“Canada’s domestic digital divide, with the North as its epicenter, has been a point of growing concern over the last several years. Much of the internet in the northernmost regions of the country is still beamed down by satellites, but a plan to link Europe and Asia with fiber optic cable via Nunavut is currently being negotiated by a Toronto-based company called Arctic Fibre.”

Picaso painting or a new iPhone 6, currency has these properties. It is:

Picaso painting or a new iPhone 6, currency has these properties. It is:

When accessing or authenticating (for example, logging into a corporate VPN or completing a credit card purchase), you are presented with a tiled screen of individual faces. I prefer a big 15×5 grid = 75 images, but Passfaces uses sequential screens of just 9 faces arranged like the number pad on an ATM.

When accessing or authenticating (for example, logging into a corporate VPN or completing a credit card purchase), you are presented with a tiled screen of individual faces. I prefer a big 15×5 grid = 75 images, but Passfaces uses sequential screens of just 9 faces arranged like the number pad on an ATM.