The blockchain is public, yet a Bitcoin wallet can be created anonymously. So are Bitcoin transactions anonymous? Not at all…

Each transaction into and out of a wallet is a bread crumb. Following the trail is trivial. Every day, an army of armchair sleuths help the FBI. That’s how Silk Road was brought down.

The problem is that some of that money eventually interacts with the real world (a dentist is paid, a package shipped or a candy is purchased at a gas station). Even if the real-world transaction is 4 hops before or after hitting the “anonymous” wallet, it creates a forensic focal point. Next comes a tax man, an ex-spouse or a goon.

The first article linked below addresses the state of tumblers (aka “mixers”). They anonymize an open network by obfuscating the trail of bread crumbs.

Mixers/tumblers aren’t the only way to add a layer of privacy to Bitcoin transactions. The Lightning Network spec includes an optional 17-hop onion routing (just like TOR’s 4 step onion routing). I have not yet seen the feature expressed in wallets or services, but if implemented, it will be even more private and trustworthy than a mixer, because there is no middle party to trust (by you) or squeeze (by investigators). It has the potential to makes any crypto Bitcoin even more anonymous than cash.

Certain cryptocurrencies (not Bitcoin) have anonymity baked in by design. Monero, ZCash and Dash are privacy tokens that use very different approaches to eliminate the bread crumbs. Monero appears to have one distinct advantage: Like the TOR network, it is trustless. But there are benefits to each approach.

Today, I was co-host of an online cryptocurrency symposium—taking questions from hundreds of visitors. A common question goes something like this:

Can Bitcoin be used in person—or is it just for internet commerce?

Our panel had a moderator, and also an off-screen video director. As I cleared my throat in preparation to offer a response, a voice in my ear reminded me that it was not my turn. The director explained that another panelist would reply. It was a highly regarded analyst and educator in Australia. Realizing that that she was calling the shots, I deferred.

I was shocked as I listened to a far off colleague suggest that Bitcoin is not useful for in-person payments. I wonder how he explains this to the grocers, tailors, lawyers, theme parks and thousands of retailers who save millions of dollars each year by accepting bitcoin—all without risk of volatility and even if they demand to instantly convert sales revenue into Fiat currency.*

“Of course it can be used in person, Numb-nut!” (I kept the thought to myself. I know better than to criticize another speaker).

An in-person transaction, such as paying for a meal after consumption, is an ideal use scenario. It benefits everyone: The seller captures greater value and the buyer is unlikely to need bank-brokered arbitration. He only needs a receipt. He will never demand a 90-day return warranty, claim that he was shipped an empty box, nor complain about the amount charged.†

But, this isn’t about my clueless colleague. It is about the ease of using Bitcoin in person and the interesting stuff that happens in the background. Let’s look at a simple purchase scenario — and then we’ll dig in to marvel at the settlement process. This is a true story, told in 7 bullets. It occurred in the summer of 2015—just 5 years after the very first use of bitcoin to purchase anything (Bitcoin Pizza Day was May 22, 2010).

It’s 2 AM on a moonlit Sunday morning. Driving from Boston to New York I rehearse the Bitcoin presentation that I will deliver at a startup clinic hosted by LaGuardia Community College and the Cryptocurrency Standards Association. I pull off the last exit in Connecticut and find the Darien Diner. My meal costs $12.

As I take one last bite of midnight quiche, I realize that I forgot my wallet! No cash; no driver’s license. I have a smartphone, but it is brand new. I have not yet loaded it with credit cards. But, I do have access to my account passwords.

I scope my surroundings. My waiter is the only one on the main floor. He is also the cashier. Seeing no other customers or staff, I figure that the owner or cook is in the kitchen; probably the only other person on premises. I approach the cash register, hoping that the waiter will accept my apology—and trust that I will pay on my return trip in a few days. Before I launch into my poor-man’s excuse, I spot the placard shown at right. Bitcoin is among the diner’s accepted payment methods!

I ask the cashier how I can pay with Bitcoin. His response catches me off-guard: “I have no idea…They told me that you would know.” What?! Does this guy recognize me? Does he know that I am on my way to give a Bitcoin lecture? This seems very unlikely. Gradually, I understand what he means, and I know what to do…

I point my smartphone at the QR code (It’s taped to the cash register next to the words: “We accept Bitcoin”). In fact, this restaurant is fully on board. I am amazed to see that a display on the register offers a custom code that is encoded with the exact meal cost. That’s really cool! So, I shift my camera to that code.

Immediately, my wallet asks if I would like to add a tip. (It’s hosted by an online exchange, but an application wallet will also work). I add $3 and press SEND.

A thermal printer next to the till spits out a narrow receipt. At the very bottom, where it would typically say “Paid with MasterCard ending in −3862”, it says “Paid with Bitcoin”. The buzzing sound of that receipt printer tells the cashier that I am good to go. Good food in the tummy and a bill has been paid. Case closed; Return to car; Drive to New York.

What Really Happened?

In the few seconds between the authorization and the printed receipt, some fascinating things occurred around the world. Seriously Fascinating! This is almost magic — and it is transforming the way payments work, and—eventually—the way we view, understand and manage cash. ‡

When I clicked SEND, a limited subset of Bitcoin credentials was presented to a massively distributed, worldwide network of miners. In effect, I informed the bookkeepers that I wish to have $15 transferred to the restaurant’s public address.

Seconds later, the original credentials were voided (this solves the ‘double spend problem’) and a new transaction was added to public ledger that we call the blockchain. It now reflects my slightly reduced wealth.

But wait! It gets even more fascinating…

The “miners” that settled the transaction and provided new Bitcoin credentials needn’t have any awareness that they just facilitated payment for a meal at a diner in Darien Connecticut. From their perspective, these individuals and large server farms in Iceland, China, Israel, and South Africa — and in college dorms spread across the world — are engaged in a massively distributed gaming competition. They are competing for rewards based on solving a math problem.

As you review that last paragraph, imagine the elegance of the global network. Imagine the power, robust nature, and benefit that comes from it’s redundant and decentralized architecture. Imagine the ongoing incentive for bookkeepers to play a critical role in balancing a world-wide ledger. Imagine that authorities cannot shut down the network or even slow it down. Imagine the trust that individuals, businesses, NGOs, banks and governments can put in the monetary supply and the mechanisms of accounting. Imagine a world where this trust benefits everyone uniformly, fairly, and without susceptibility to graft or inflation.

Bitcoin and the blockchain, introduced together, are not minor, incremental contributions to economics, bookkeeping, trust, and commerce. They are overwhelmingly significant contributions to the future of human society and its institutions.

† You may have heard that bitcoin transactions are immutable. This is a simplification. The public ledger is immutable, but transactions are reversible, if terms are clear to both parties. Just as with Ethereum, smart contracts are built into the technology. So are hooks to centralized mediation, if that’s what the agreement calls for. Charge-backs, refunds, warranty demands and other arbitration are all possible. These features are built into Bitcoin, but rarely used in this early era.

Most Bitcoin transactions today are payments; they are not charges. Although they do not typically accommodate bank-brokered returns, rescission and charge-backs, these are all possible, and often without requiring an authority to broker the dispute.But these traditional safeties or mitigation must be agreed upon in advance. No longer does the seller have all the power, or the buyer need to run to a credit card processor to complain. Sales are either immutable or brokered by a 2-party contract.

This is not your grand-daddy’s payment mechanism. It is so much more evolved!

‡ In 2017, Bitcoin went through a period of intense growing pain. Transactions became so slow and costly, that in person transactions became impossible, especially for any amount less than $500. If you needed a transaction to complete in less than an hour, you would need to enlist in a bidding contest. A quick confirmation could cost upwards of $30 US.

The restaurant payment related above was an on-chain transaction. Today, transactions that use the Lightning Network overlay may occur within a private channel apart from the blockchain. But ultimately, every change in bitcoin ownership results in an individual or aggregated entry onto the blockchain.

Crisis in late 2017 and 2018

Sadly, in researching this article, I learned that the Darien Diner no longer accepts Bitcoin. Problems associated with transaction cost and delays in 2017~2018 discouraged acceptance by a great many retailers. No one eating a $12 meal would ever pay $30 in fees, and a cashier is not going to wait 2 hours to validate payment from a customer who has already eaten a meal and wants to hit the road.

That glitch sparked a terrible reversal of retail adoption. Even now (Q3 of 2019), retail penetration is sharply off its peak. We are barely beginning to recover the early adoption rate. Vendors lost faith, and many don’t yet realize that their POS investment can now be safely be reactivated. Lightning Network to the rescue!

he Next Crisis

Another crisis is looming, but it too will be solved.

Although the Bitcoin network is fast and inexpensive, the proof-of-work method used by miners to arrive at a distributed consensus consumes far too much power to scale. Mass adoption would consume more power than the world currently generates.

And here’s the kicker: The mining incentive ensures that any new, inexpensive energy that might be discovered in the future would be gobbled up by miners with no additional benefits to society (or even to the Bitcoin network). All the new, free (or cheap) power would be diverted away from homes, businesses, manufacturing and public works. The incentive for grabbing every cheap watt is very much like a cancerous growth.

Clearly, this is not sustainable. Bitcoin mining already uses more power than all of Argentina. But great minds are working on the problem and alternative methods of guaranteeing a fair, crowd-sourced accounting consensus are being tested, analyzed and debated. We will get through this complex problem, and hopefully—this time—without demoralizing a key factor in the tetrad: Consumers, developers, vendors & miners.

This afternoon, an automated bot at Quora suggested that I answer a reader question. Quora is essentially an “Ask the expert” web site. It is the world’s largest, cataloged and indexed Q&A repository.

This is the question I was asked to answer:

Some pundits believe Bitcoin is a fad, while others seem to feel that it is better than sliced bread. I like sliced bread.* Is Bitcoin really that cool? —Or is it just a lot of Geeky hype?

One other columnist answered before me. Normally, I pass on an invitation, if a question has already been answered. But in this case, the individual answering the question has yet to see the light. He has wandered into the Church of the Blockchain, but he just didn’t realize that the man sweeping the floor is the prophet.

Here then is my answer, regarding Bitcoin, the blockchain and sliced bread…

I respectfully disagree with Jim Euclid. He answered this question too. Perhaps it is arrogant of me to state with confidence that he will change his mind, if he is still around in another 30 or 40 years. So will everyone reading this.

Bitcoin and the blockchain were introduced together in a white paper by a quasi-anonymous developer in October 2008. He or they used a pseudonym, but communicated with a broad group of developers before and after unveiling the solution to an age old problem of math, logistics and cryptography.

Just over 1 year later, Bitcoin began moving between individual owners. And then it began to re-write the history of economics, bookkeeping, consensus, trust and the very democracy that is so precious to us. It is changing what we understand about so many things. But its true contributions have barely even begun.

Bitcoin is as ‘cool’ an invention as there can be. Like the steam engine, vacuum tube, automobile, television and the internet, it is radically transformative. Each of these inventions has (or will) contribute enormously to human progress and happiness.

The problem that Satoshi solved goes back to Aristotle and has profound social implications for the future of humanity. There is no poetic license or potential for overstating the importance of both Bitcoin and the blockchain. It will impact your life—probably in very positive ways—with a punch that matches the rise of agriculture, indoor plumbing or airline travel.

Sorry, Jim. I respect your opinion, but I see the future a bit more clearly than you. The internet is a vehicle. It is certainly important. But it is only the highway. Bitcoin is the marvel that the internet’s instant, inexpensive and ubiquitous communication was meant to spawn.

I have always felt pride over the fact that I was alive when man first landed on the moon. I was a child and I had nothing to do with that achievement—but somehow, I am gratified that this event intersected with my life.

Unlike the moon landing, Bitcoin has no Jules Verne or cave paintings from past generations yearning to conquer something that is tangible. We have only Aristotle’s insight that money was not yet perfect—and his recognition that issues of democracy and governance seem to have insurmountable impediments. But the problems that Bitcoin and the blockchain address are just as real as the moon overhead. And the solutions they will spawn are even more relevant to our civilization.

I have even more pride that I have witnessed the birth of decentralized, permissionless, distributed consensus—and specifically Bitcoin. It will impact my health, wealth and happiness even more than everything that NASA and space technology have spawned.

Am I smug that I recognized the importance of Bitcoin and the blockchain just 4 months after its unveiling? You bet I am! And even if Jim doesn’t recognize it yet, someday I will rub this fact in his face.

(Kidding…but it is personally comforting to be on the right side of history!)

* Note: In America, the expression “sliced bread” refers to something that is really clever, desirable and coveted. It is often paired with the word “since” like this: That new iPhone is the best thing since sliced bread.

The future of the legal industry is being reshaped by a number of rapidly advancing technologies and the disruptive ideas they enable.Today’s lawyers are beingadvised to learn to code, develop an artificial intelligence (AI) application,andoutsource discovery to machines.Of the many new technological drivers impactinglaw firms is the secure information exchange platform known as blockchain.Some see it as a the basis for the reinvention of economies while others simply see it as means of secure and incorruptible information exchange between counterparties. This cloud-based distributed ledger technologyprovides a source of irrefutable record of every transaction. In legalit is enabling fully automated self-executing “smart” contracts, and has the potential to help attorneys provide new services and create new value for clients and law firms.Blockchain is known as the structure underlying Bitcoin and other digital currencies, but its applications inthe legal sectorare still evolving.This article provides an overview of the technology, highlights example applications and case studies, and presents a possible timeline of future developments over the next decade or so.

Overview:Blockchain and Bitcoin

Blockchain and Bitcoin have gained notoriety lately as a potential solution to an outdated and burdensome system for managing financial transactions between counterparties. Today most financial transactions between counterparties are settled via financial intermediaries which adds time and cost to the settlement process. Blockchain offers a distributed ledger model whereby the parties settle directly with each other, the transactions are recorded, secure, and immutable, and the counterparty identities remain anonymous. The goal is to enable a simplified and trustworthy financial ecosystem- but these digital peer-to-peer networks, also challenge the authority of institutions (banks, regulators, and governments) and are thus creating disruption.

According to its advocates, the decentralized nature of blockchain and Bitcoin will cause much-needed disruption, with reverberations far beyond the financial realm. There is an element of social revolution in blockchain, thus it is often portrayed as a conduit for challenging the status quo. Though Bitcoin, a digital currency, is an explicitly financial innovation (i.e., for payments, transfer of funds) blockchain is far less specific. Blockchain serves a critical role in the administration of Bitcoin, and that of other digital currencies, but it can actually be used to complete other objectives and track the movement, transfer, and ownership of all sorts of things besides money (examples include luxury goods, education credits, property titles, and patents, to name a few). Though blockchain is structured like a traditional accounting tool—it’s fundamentally a ledger that tracks deposits in and payments out, and maintains a running balance—its uses go far beyond counting coins.

Lest we assume blockchain and Bitcoin are solely the tools of the far-left, libertarian, anarchists, and socialists among us, this technology has captured the attention of global business and industry to the tune of millions of dollars. Among banks alone, one source projects spending on blockchain solutions to grow to over $200 million in 2017, $300 million in 2018, and $400 million in 2019. Perhaps ironically, a great wave of enthusiasm for blockchain now emanates from the business establishment, including stalwarts like banking, finance, real estate, and law.

Applications to Law Firms

While the basic metaphor for blockchain is an automated checkbook register that instantly reconciles transactions, several concepts are inherent to blockchain which are ideally suited for applications to law firms. Current legal industry activity around blockchain ranges from the simple—payment for services rendered, verification of contracts, representing companies conducting business on the blockchain—to the highly complex—formulation of an entirely new legal system altogether. Regarding the latter, which would usurp local or national laws to create a globally agreed upon set of codes that govern rights during a dispute, one can see how incredibly large-scale blockchain’s legal applications could potentially become. In terms of contracts and payments, though, the firms now adopting blockchain are attracted to its practicality: it reduces the resources needed to complete day-to-day operations. For example, Goldman Sachs estimates that $11 to $12 billion per year could be saved with blockchain-based clearing and settlement of cash securities, and $2 to $4 billion yearly savings from moving real estate titles to distributed ledgers.

A growing number of industry examples demonstrate the diversity of applications of blockchain and bitcoin to legal services:

International law firm Steptoe & Johnson helps clients in all industries manage application of the blockchain in their businesses, and accepts Bitcoin as payment for fees.

King & Wood Mallesons (headquartered in Hong Kong) has more than a few dozen lawyers who have a focus on blockchain, including smart contracts.

Perkins Coie LLP partner Dax Hansen (US) launched the first blockchain legal industry practice in 2013, which has grown to over 40 lawyers focused on blockchain technology, digital currencies, and distributed applications of all types.

Selachii (UK) will implement self-executing smart contracts on blockchain, starting with wills, title registries, and shareholder agreements.

Allens (Australia) wrote a report suggesting that the future of the legal business model, which profits from an absence of trust between organizations, is imperiled by the rise of blockchain technology.

Outside of law firms themselves, the startup ecosystem is packed with examples of services geared toward marrying procedural business practices with blockchain:

Juro uses blockchain technology to underpin the creation and signing of legal contracts.

The Decentralised Arbitration and Mediation Network (DAMN) operates as a network of smart contracts on the Ethereum blockchain creating an “opt-in justice system for commercial transactions” as a new form of cross-border dispute resolution.

CommonAccord is creating global codes of legal transactions, automating legal documents such as master service agreements.

DAO.LINK is an initiative which facilitates brick-and-mortar business interactions with blockchain-based organizations.

Timeline of Possible Future Blockchain Developments in Law

Next 3 years

DAOs: Distributed autonomous organizations with no workers and no bosses, just algorithms.

Merger and acquisition on “auto pilot”.

Elimination of some jobs and roles (banker, advisor, lawyer).

Merging AI and blockchain; robolawyers on blockchain.

Next 5 years

DAMN – a global legal system for international dispute resolution.

Automated arbitration, dispute resolution, and various legal and banking processes eliminating more roles in law firms and banks.

Creation of new professional roles to deal with legal ramifications of blockchain.

5–10 years

Algocracy: Law is code, code is law.

DAS: distributed autonomous societies with automation of services, justice, rights, and laws.

Blockchain and cryptocurrency have gained unprecedented ground. The central bank of China is piloting a blockchain-based cryptocurrency, a very loud signal about the rising status of the technology which will legitimize its use. Another recent indicator came in the form of headlines screaming about Bitcoin’s price trends, earning investors millions.As futurists, we expect that for every big wave of change there are dozens of small ripples; the revolutionary nature of Bitcoin and blockchain means it will disrupt businesses of all kinds. Because it involves money, contracts, and ownership, this is a special consideration for lawyers and firms.

Starting now, law firms owe it to their staffs and teams to begin a conversation about blockchain, Bitcoin, and other digital currencies. Information, in this case, is power—blockchain’s distributed disruption of banks, laws, and most traditional social institutions will generate new conflicts, anxieties, and tensions for which legal remedy will be the only solution. It is a likely topic of future legal matters.

Keep in mind that the best way of describing blockchain is “distributed,” in other words, absent of central authority. A lot of the projects in the works seek to apply this thinking to society at large through distributed autonomous societies (DAS) and distributed legal systems. If a distributed mindset prevails, this will concern lawyers, judges, law enforcement, and anyone in occupations that rely on a centralized legal system.

Furthermore, the entire basic model of business conduct stands to be disrupted on the same scale as it was during the rise of the internet as a business tool—blockchain, in combination with other technologies like artificial intelligence and cloud computing—will eventually transform the very basis of business and productivity, possibly even money itself. By decentralizing the powers that be, blockchain seems to be the high-tech disruption that will challenge law at every level and function.

ABOUT FAST FUTURE

Fast Future publishes books from future thinkers around the world exploring how developments such as AI, robotics, and disruptive thinking could impact individuals, society, and business and create new trillion-dollar sectors. Fast Future has a particular focus on ensuring these advances are harnessed to unleash individual potential and enable a very human future. See: www.fastfuture.com

Rohit Talwar is a global futurist, keynote speaker, author, and CEO of Fast Future where he helps clients develop and deliver transformative visions of the future. He is the editor and contributing author for The Future of Business, editor of Technology vs. Humanity and co-editor of a forthcoming book on Unleashing Human Potential—The Future of AI in Business.

Alexandra Whittington is a futurist, writer, faculty member on the Futures programme at the University of Houston, and foresight director at Fast Future. She is a contributor to The Future of Business and a co-editor for forthcoming books, Unleashing Human Potential—The Future of AI in Business and 50:50—Scenarios for the Next 50 Years.

To highlight the possibility of risks to banking and finance sectors arising from new financial instruments based on blockchain technology; primarily from novel financial accounting methods and products called “stablecoins,” digital tokens, and cryptocurrencies.

To encourage regulators and policymakers to engage blockchain thought leaders, product developers and the community in general to better understand the economic and policy implications of public, private and permissioned blockchains; their application to banking and finance regulations; and how innovation may be encouraged in a safe, sound and responsible manner.

Like any technology, blockchain can and may be used to improve a variety of operational, identity, security and technology challenges that the future of digital banking, business and society face. Blockchain technology is also poised to create new and increasingly clever methods and economies for value, commodities, assets, securities and a slew of yet-to-be discovered financial instruments and products. However, no leap in technology and finance is ever made without risk. As policymakers and stewards of the current and future digital economy and ecosystem, we have an obligation to our constituents and the global banking and finance community to guide the growth and adoption of emerging fintech technology in a safe and sound manner.

To that end, three areas that have the potential for regulatory and compliance issues as companies such as JP Morgan Chase, embrace and develop blockchain technologies to leverage digital tokens, cryptocurrencies and novel accounting systems such as the so called “JPMCoin,” are highlighted:

Stablecoin — The industry needs a common definition. There is presently not an industry definition of a stablecoin, digital token, or cryptocurrency. Before it is even possible for governmental agencies to draft useful regulations the industry must come up with common definitions. We believe that establishing a common definition is an important step to growing a rich and innovative framework and sandboxes for not only novel blockchain applications but other emerging fintech technologies.

Fractional Reserve Banking and Stablecoins — How will cryptocurrencies, digital tokens and stablecoins be treated in an ecosystem of fractional reserve banking? Much like the introduction of collateralized debt obligations, synthetic credit default options and other novel, complex financial instruments, the introduction of institutional “stablecoins” and digital tokens may present hereunto unknown risk. As technology evolves to facilitate machine learning, artificial intelligence, high speed frequency trading and novel blockchain applications such as “stablecoins,” careful consideration should be given to how these blockchain applications (and other emerging technology) may unintentionally encourage risky behavior that creates systemic financial risk and operational risk that undermines confidence in markets.

Operational Safety & Soundness — The creation of institutional stablecoins, digital tokens and cryptocurrencies poises new financial safety and compliance questions. From the basic, “How is the value of these stablecoins determined?” to: “What are the standards for digital token custody?”. To the more complex questions of: “Can the terms stablecoin, digital token and cryptocurrency be used interchangeably?” to: “How will these instruments be reflected on company balance sheets, managed day-to-day in accounting systems and taxed?”

Conclusion

Emerging technology such as blockchain promises great leaps in operations, transparency and accountability. However, as we prepare to leap headlong into these technologies we should also consider where we will land.

We encourage regulators and policymakers to engage banking, technology and compliance leaders to better understand the implications of private-permissioned decentralized ledger technology (aka blockchain) and what steps we can take now to encourage and enable innovation, while also landing safely in the future of banking, finance and an electronic cash-less ecosystem.

I love hearing the enthusiasm and joy in the voices of first time home buyers who are going to save money, bond and remodel their house together. Brand new doctors, seasoned lawyers, accountants, project managers, the boldest of GenX and Millennials who grew up swinging VR joystick in lieu of hammers. But they’ve watched Property Brothers and Love It or List and have the best database of YouTube videos for home remodeling in their entire subdivision or building. They even park in the “Pro” section at Home Depot and have their very own monogrammed Leatherman construction gloves.

You can remodel your own home. Even “just” your kitchen or “just” your bathroom. You can read and have all the resources at your disposal. But don’t. Don’t even fucking think about it. Remember how you tried to cook Thanksgiving dinner last year and ended up burning up your kitchen, which is why you need to replace it? Those were simple enough directions too, right?

But what does this have to do with blockchain and more importantly your business?

Glad you asked. Well, your business is like your house. Blockchain is like a remodel. You can do it yourself. You’re after all a pro at your business. But your business isn’t blockchain. Your business is shipping, consulting, farming, logistics, banking, money exchange, insurance, lending, maybe even selling pizzas. Your business is a business. Your business isn’t a way of doing business or a business tool like blockchain. Your business is a way of generating you income to provide for your family, workers, community, financial security and future. It ain’t a way to decentralize any of those, unless you want to find out what a “decentralized” retirement looks like. (Hint, think working poor at 75 years old. #GigEconomy).

So! Before you decided to attempt to blockchain your business, ask yourself, “Could I remodel my house?” 99.99% of the time the answer is “Fucking, hell, no!” You should no more attempt to “blockchain” your business than you should remodel your house. So what do you do?

Hire a professional

Can’t afford one? Then you’re not ready to remodel your house or “blockchain” your business.

By the way, do you even know what the fuck “blockchaining your business” even is? I’m like an expert in this industry and I don’t recommend 99% of businesses “blockchain” any part of their business. Cause did you know you can “blockchain” parts of your business operations, functions and processes and not the entire business? I’ll tell you a secret, blockchain is just a tool you use to do your business. It ain’t a business itself, a panacea for customer acquisitions or guarantee of increased sales or revenue. It’s like a hammer that’s shiny and brand new, but in your hands it’s more likely to tear giant holes in your business’ model, customer base and revenue streams.

So, like you would a plumber, carpenter or WiFi guy, before you go to “blockchain your business” hire a professional. Cause the funny part is once (if) you blockchain your business, then you’ve got to run your business. Remember, blockchain isn’t your business. Your business is. Don’t allow the hype of DIY tech nerds get you wild with excitement leaving you swinging a proverbial sledge hammer through your internal operations and revenue streams.

Hire a professional. And much like building a house, don’t start by hiring a painter to lay the foundation. Hire a General Contractor to guide you through the process. And whatever you do, do not let the plumber and electricians (coders and programmers) charge you by the hour. As then, it’ll take three times as long, cost 10 times as much and your odds of being electrocuted when you drop a deuce are high.

Who is a “Blockchain General Contractor”? Axes and Eggs of course.

Blockchain plumbers, carpenters, electricians, painters, engineers and designers: Chainhaus — they’re your one stop shop. But you can always go to the Home Depot of Blockchain Deloitte Ireland.

Fly by night, Tim the Tool man, unpermitted, lien inclined, blockchain enthusiast.… On the advice of our legal counsel (www.cogentlaw.co) I won’t name those decentralized con artist. But they probably showed up to give you an estimate driving a Lamborghini and offered you custom views of the moon. So you know who they are.

Conclusion

Stick to your business. It’ll ultimately make you more money.

Oh, and if you need a real Construction General Contractor, visit www.mattbeth.com

My name is Samson. I’m an Adjunct Professor at Univ of New Hampshire School of Law, human and an anthropologist at Axes and Eggs, a Washington, DC based Think Tank and digital advisor. If you like what you read, share it! If you disagree, share what you know or how you feel in the comment section below. Feel free to hit me up on Twitter or Instagram @HustleFundBaby or follow me onLinkedIn. Finally, I would say thoughts are my own but I probably stole them from a woman.

I owe Jack Shaw a favor. It’s one of those, “This one time in Cambodia…” type of favors. We won’t speak of it beyond perhaps a nod and wink. It’s not written down anywhere; the details of such are so vague as to be almost non existent, while encompassing the known universe. It expires upon death, of the sun; and can be redeemed whenever and by another person who need only walk up to me and say, “Jack Shaw sent me. He says to tell you ________”. And tada, that favor has been redeemed for value.

Jack would call this favor a “marker.” It’s more valuable than your house, the Empire State Building & 100k Bitcoins combined. It can even be redeemed for something even more precious, my time or an opportunity or access to my network. You know, those things that money can’t buy. Well, you can lease my time from time to time.

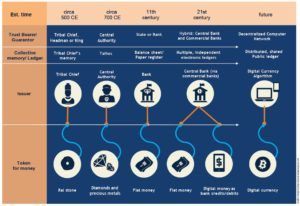

Favors, markers and promises are humanities’ first virtual currencies.

They’ve gone digital recently, as Jack might redeem his marker via a WhatsApp or WeChat text message.

Favors and promises aren’t financial obligations per-say. They’re moral debts that can be redeemed for things of intrinsic, monetary, social and/or actual value. Now, here is where things get a little weird. The thing about “money” is that it doesn’t have any value. It’s actually a reflection of a moral debt. Hence why the US dollar is backed by the “Full Faith and Credit of the US Government” and not say, gold or wheat. You believe…that people will feel obligated to pay taxes and in turn the government will collect these social obligations (aka favors) for the good and benefit of The People. This moral obligation is part of that “Debt to Society” you’ve heard so much about, are obligated to pay, but don’t recall actually signing up for.

Long ago, these virtual currencies of favors, promises, social obligations and credits were turned into what we now regard as money. Not because paper money or coins had or have any intrinsic value, but because for trade beyond one’s family or clan, it’s easier to convey/store and document the value of Sam owing you two chickens, using cash as that documentation (or store of value). As you extended to him a two chicken line of credit.

“Credit” is just another favor or marker with terms.

Coins and “Banknotes” (because people wrote down how much credit they gave you) were just the earliest form of noting and coming to consensus on how to document these virtual currencies of favors, markers, promises and credit.

Overtime, what favor or credit money represents has been lost. We’ve been conditioned to simply believing (Full Faith and Credit) that paper money has intrinsic value, when it simply doesn’t.

Paper money isn’t backed backed by anything other than your faith.

Hence why inflation is such a troublesome concept for most. It challenges the fundamental principles of your faith — every time the government prints more paper money. It extends to itself (and then to you, via banks) made up and virtual favors by the billions. They are favors and markers with no value behind them; lines of credit with no chickens attached. So when these virtual chickens come home to roost, as actual value, guess what? There aren’t any chickens, just a whole lotta hungry believers.

Everybody believes in this system of virtual currencies of credit, favor and marker collection, except the banks and the corporations who effectively pay zero in taxes, while simultaneously collecting trillions in credits from people and then turning those virtual dollars into “real wealth.” Think real estate.

Fun fact/Tangent: Why is real estate called “real?” Hint: It has something to do with the fact that money has no value (isn’t real) but shelter/housing does. We’ll talk about how banks and corporations got out of their social contract at your expense later.

In conclusion, as we’ve a lot to consider now, virtual currencies aren’t anything new. They’re as old as favors and promises. Digital money (much like paper money) doesn’t actually exist. It’s actually easier to “print” digital dollars than paper dollars. One requires paper and ink. The other? Well, just add another few zeros and tada! #InstantCash!

So do me a favor…next time someone tells you that Cryptocurrencies are a sham, smile at them because you now know that money has no value and the government can make as much money up out of thin air (with a side of faith) as it can add zeros to a ledger. Then, ask him/her if you can borrow two live chickens. You promise to pay them back. 😉

My name is Samson. I’m a Professor of Blockchain at Univ of New Hampshire School of Law, human and an anthropologist at Axes and Eggs, a Washington, DC based Think Tank and digital advisor who answers your questions when Google can’t. If you like what you read, share it! If you disagree, share what you know or how you feel in the comment section below. Feel free to hit me up on Twitter or Instagram @HustleFundBaby or follow me on LinkedIn. Finally, I would say thoughts are my own but I probably stole them from a woman.

At Quora.com, I respond to quetions on Bitcoin and Cryptocurrency. Today, a reader asked “Will we all be using a blockchain-based currency some day?”.

This is an easy question to answer, but not for usual Geeky reasons: A capped supply, redundant bookkeeping, privacy & liberty or blind passion. No, these are all tangential reasons. But first, let’s be clear about the answer:

Yes, Virginia. We are all destined to move, eventually, to a blockchain based currency.

I am confident of this because of one enormous benefit that trumps all other considerations. Also, because of flawed arguments behind perceived negatives.

Let’s start by considering the list of reasons why many analysts and individuals expect cryptocurrencies to fail widespread adoption—especially as a currency:

It lacks ‘intrinsic value’, government backing or a promise of redemption

It facilitates crime

Privacy options interfere with legitimate tax enforcement

It is susceptible to hacks, scams, forgery, etc

It is inherently deflationary, and thus retards economic growth

It subverts a government’s right to control its own monetary policy

All statements are untrue, except the last two. My thoughts on each point are explained and justified in other articles—but let’s look at the two points that are partially true:

Indeed, a capped blockchain-based cryptocurrency is deflationary, but this will not necessarily inhibit economic growth. In fact, it will greatly spur commerce, jobs and international trade.

Yes, widespread adoption of a permissionless, open source, p2p cryptocurrency (not just as a payment instrument, but as the money itself), will decouple a government from its money supply, interest rates, and more. This independence combined with immutable trust is a very good thing for everyone, especially for government.

How so?…

Legislators, treasuries and reserve boards will lose their ability to manipulate the supply and demand of money. That’s because the biggest spender of all no longer gets to define “What is money?” Each dollar spent must be collected from taxpayers or borrowed from creditors who honestly believe in a nation’s ability to repay. Ultimately, Money out = Money in. This is what balancing the books requires in every organization.

This last point leads to certainty that we will all be using a blockchain based cryptocurrency—and not one that is issued by a government, nor one that is backed by gold, the dollar, a redemption promise—or some other thing of value.

Just like the dollar today, the value arises from trust and a robust two sided network. So, which of these things would you rather trust?

a) The honesty, fiscal restraint and transparency of transient politicians beholden to their political base?

b) The honesty, fiscal restraint and transparency of an asset which is capped, immutable, auditable? —One that has a robust two sided network and is not gated by any authority or sanctioned banking infrastructure

Today, with the exception of the United States Congress, everyone must ultimately balance their books: Individuals, households, corporations, NGOs, churches, charities, clubs, cities, states and even other national governments. Put another way: Only the United States can create money without a requirement to honor, repay or demonstrate equivalency. This remarkable exclusion was made possible by the post World War II evolution of the dollar as a “reserve currency” and the fractional reserve method by which US banks create money out of thin air and then lend it with the illusion of government insurance as backing. (A risky pyramid scheme that is gradually unravelling).

But, imagine a nation that agrees upon a form of cash that arises from a “perfect” and fair natural resource. Imagine a future where no one—not even governments—can game the system. Imagine a future where creditors know that a debtor cannot print paper currency to settle debts. Imagine what can be accomplished if citizens truly respect their government because the government lives by the same accounting rules as everyone else.

A fair cryptocurrency (based on Satoshi’s open-source code and free for anyone to use, mine, or trade) is gold for the modern age. But unlike gold, the total quantity is clearly understood. It is portable, electronically transmittable (instant settlement without a clearing house), immutable—and it needn’t be assayed in the field with each transaction.

And the biggest benefit arises as a byproduct directly of these properties: Cryptocurrency (and Bitcoin in particular) is remarkably good for government. All it takes for eventual success is an understanding of the mechanism, incremental improvement to safety and security practices and widespread trust that others will continue to value/covet your coins in the future. These are all achievable waypoints along the way to universal adoption.

Maria Bustillos is founder of the blockchain supported publication, Popula. I stole the title of this post from her essay at Medium.com (linked below).* I hope that Maria considers it a tribute rather than title-plagiarism. Her article is blocked by a pay wall, so allow me to explain a concept that confounds even a Nobel Prize winning economist. My take on the issue is somewhat different than Ms. Bustillos.

The difficulty understanding or appreciating Bitcoin boils down to a misconception that the dollar is backed by something more tangible, such as gold, guns or the promise of redemption. Not only is this an illusion, but Bitcoin is backed by something far more tangible, intrinsic and durable.

The illusion that “real” value emanates from government coupled with a robust consumer economy has been woven into our DNA for millennia. But, the value we attribute to a Dollar, Euro, or Yuan is a result of conditioning rather than any intrinsic value. That same conditioning has led us to believe that there is something sane and inherent in a nation that controls its money supply and its monetary policy.

Most public works projects—power generation, space ships, or the telephone network—were controlled by government in the past. If not, they were regulated as a licensed monopoly. This creates a choke point, a lack of competition, and a gaping opportunity for inefficiency, mismanagement or graft. It defies a free market economy and it concentrates power in the hands of politicians. But, at one time, it seemed necessary.

You might assume that government controlled these industries because they relate to areas of critical infrastructure and public welfare. That’s part of it, but it’s not the real reason. In each sector, a distributed or free market solution was prevented due to technology limitations or issues of scaling and geography.

Government issued money exists because in the past, we had no mechanism to arrive at a consensus on the value of something that is portable, fungible, secure, anti-forgeable and easily transmitted. Not even Gold fits the bill (pun intended). Prior to 2009, the only thing that met the criteria for money in a modern society was government issued fiat. At least someone, somewhere said that this is money and that this is what we must use to pay our taxes.

Today, there is no more reason for a government to control its money supply than there is for it to control communication networks, space travel or package delivery services. Today, a free and competitive marketplace benefits all of these industries and even government itself. And here’s the kicker: No harm will come to a government that uses a completely trusted, transparent and decentralized currency, rather than firing up a printing press whenever a group of transient politicians spends beyond their means.

The economic order facilitated by the blockchain is not as radical as it seems. Aristotle sought to solve the double-spend problem and lamented the lack of an accounting tool that we can now address via the clever combination of encryption and a communications network that is both instant and ubiquitous.

I am not smarter than your average bear, nor am I clairvoyant. But once in a while, I recognize a truth before the masses—and before its time. It’s time to clearly and succinctly illuminate business, banks, consumers, creditors and government:

1. The value we attribute to the dollar is an illusion

2. Bitcoin is not just fair and cost effective. It is tangible and durable. It is good for consumers and good for governments.

Bitcoin ushers in an era of accountability and more fairness. It does not facilitate crime, nor interfere with a government’s ability to tax, spend or enforce tax collection.

Bitcoin is a cryptocurrency with a firmly capped supply. Will it lead to deflation? Could governments lose control over their own monetary policy? Yes to both questions…

But, these are each good things. Capping the money supply and decoupling a nation from monetary policy not only eliminates inflation—it increases access to capital, retires debt more quickly, reassures creditors, imposes transparency and honesty—And it accelerates economic growth, rather than retarding commerce.

Dispelling three millennia of conditioning can be confusing and unsettling. I hate understanding something before my peers. Let’s please get ahead of the curve on this one. I want to enjoy the benefits of using real money in my lifetime.

* I wrote the first article more than 7 years ago. It is a simple explanation of a geeky, new economic mechanism. Bitcoin had not yet entered mainstream media nor gained attention of Wall Street investors. But consider the similarity to Maria’s tutorial in the 2nd article. Perhaps Maria and I think alike!

The Disruption Experience this Friday in Singapore is a blockchain event with a difference. With apologies to the Buick commercial, this is not your grandfather’s conference…

I know a few things about blockchain conferences. I produced and hosted the first Bitcoin Event in New York. My organization develops cryptocurrency standards and practices. We help banks and governments create policy and services. And as public speaker for a standards organization, I have delivered keynote presentations at conferences and Expos in Dubai, Gujarat India, Montreal and Tampa, New York and Boston.

Many individuals don’t yet realize that both Bitcoin and the blockchain are as significant as the automobile, the transistor and the Internet. I was fortunate to grasp Bitcoin and the blockchain early in its history. It is never boring to help others understand the blockchain.

And so, I am an evangelist for both a radically improved monetary system and a transformative tool. During the past eight years, I have honed the skill of converting even the most profound skeptic. Give me 45 minutes in front of any audience—technical, skeptical or even without any prior knowledge—and I will win them over. It’s what I do.

An Atypical Conference Venue

As Bitcoin and altcoins begin the process of education, adoption and normalization, the big expos and conference events have begun to splinter and specialize. Today, most blockchain events market their venue to specific market sectors or interests:

For me, Smart Contracts are one of the most exciting and potentially explosive opportunities. As a groupie and cheerleader, I am not alone. Catering to the Smart Contract community is rapidly becoming a big business. Until this week, I thought it was the conference venue that yielded the biggest thrills. That is, until I learned about the Disruption Experience…

Few widely promoted, well-funded events address the 600 pound elephant in the room: What’s the real potential of blockchain trust, blockchain economy or blockchain AI? Take me beyond tokens and currency (please!). How can an international event help us to realize the potential of a radical new approach to accounting, trust and arbitration? Let’s stop arguing about Bitcoin, Ethereum or ICOs…

How can we unleash the gorilla—and grease— a fundamental change that benefits mankind, while providing leapfrog technologies for us?

—At least, that’s my spin on the potential of an unusually practical venue.

That question is slated to be answered on Friday at a big event in Singapore. And get this—It is modestly called a “Sneak Peak”. This is what I have been waiting for. The Disruption Experience premiers on September 28 at the V Hotel Lavender in Singapore. But don’t show up at the door. This event requires advance registration. (I do not offer a web link, because I hate being a conference huckster. If you plan to be in the area at the end of this week, then Google the event yourself).

What’s the big deal?

The Disruption Experience team is populated by blockchain developers, educators and trainers who take issue with existing events that focus on monetization. The purity of intention was overrun by greed. And so, they set out to form an event with a more altruistic purpose: Build technology, relationships, mechanisms and educational tools that better mankind. The focus at this event and the conferences that follow is to educate, expose and innovate. The focus is squarely on disruptive technology.

With their team of blockchain innovators focused on benefits and progress, I suspect that attendees will get what we have been searching for: Education, investment opportunities, an edge on new technologies and job opportunities.

Cusp of a Breakout Year

As an analogy, consider the race to understand Bitcoin and consider the engines & motors.

Bitcoin and the blockchain were introduced simultaneously in a 2009 whitepaper. It’s a bit like explaining the engine and the automobile together—for the very first time. One is a technology with a myriad of applications and the potential to that drives innovation. The other is an app. Sure, it’s useful and important, but it’s just an app.

For 8 years, Bitcoin was a radical and contentious concept. Of course, there was the mystery of Satoshi and an effort to pinpoint his or her identity. And, a great debate raged about the legitimacy and value of decentralized, ethereal money. But, the interest was reflected primarily on the pages of Wired Magazine or at Geek-fests. Bitcoin was complex and costly to incorporate into everyday purchases and there were questions and gross misconceptions about hacking, regulation, taxes, criminal activity. The combined audience of adopters, academics, miners and geeks was limited.

That changed last year. With serious talk of exchange traded funds, a futures and derivatives market began to take shape. A critical operational bottleneck was addressed. Ultimately, 2017 was a breakout year for Bitcoin. You may not be using it today, but the smart money is betting that it will enhance your life tomorrow—at least behind the scenes.

Likewise, 2019 is likely to be the breakout year for blockchain applications, careers, products and—perhaps most importantly—public awareness, understanding and appreciation. Just as motors and engines are not limited to automobiles, the blockchain has far more potential than serving as an engine for decentralized cash. It is too important to be just a footnote to disruptive economics. It will disrupt everything. And we are the beneficiaries.

What is Interesting at The Disruption Experience?

The Friday event in Singapore covers many things. The presentations and tutorials that quicken my pulse relate to:

AI

Smart Contracts

Serious insight into blockchain mechanics, applications, adoption, scalability and politics

There’s even an exciting development in ICOs…

If you read my columns or follow my blog, then you know I am not keen on initial coin offerings (ICOs). That’s putting it mildly. They are almost all scams. But a rare exception is the Tempow ecosystem which encompasses three functional tokens. Stop by their exhibit and meet the officers of a sound economic mechanism that facilitates decentralized trading while overcoming the efficiency paradox.

What can I do at Disruption Experience?

The September 28 event is a preview for January’s Inaugural Event.

Listen and learn what Disruption is all about

Experience the first Virtual Reality Expo

Get to know the speakers and founders of Disruption

Hear about the Disruption Utility Token (DSRPT Token)

Meet the Disruption Team

See Disruption Expos

… and much, much more.

If you get to the big event, be sure to find the organizer and host, Coach Mark Davis. Tell him that I sent you. His passion and boundless enthusiasm for the blockchain and especially for transformative disruption is quite infectious.

For me, Smart Contracts are one of the most exciting and potentially explosive opportunities. As a groupie and cheerleader, I am not alone. Catering to the Smart Contract community is rapidly becoming a big business. Until this week, I thought it was the conference venue that yielded the biggest thrills. That is, until I learned about the Disruption Experience…

For me, Smart Contracts are one of the most exciting and potentially explosive opportunities. As a groupie and cheerleader, I am not alone. Catering to the Smart Contract community is rapidly becoming a big business. Until this week, I thought it was the conference venue that yielded the biggest thrills. That is, until I learned about the Disruption Experience… The Disruption Experience team is populated by blockchain developers, educators and trainers who take issue with existing events that focus on monetization. The purity of intention was overrun by greed. And so, they set out to form an event with a more altruistic purpose: Build technology, relationships, mechanisms and educational tools that better mankind. The focus at this event and the conferences that follow is to educate, expose and innovate. The focus is squarely on disruptive technology.

The Disruption Experience team is populated by blockchain developers, educators and trainers who take issue with existing events that focus on monetization. The purity of intention was overrun by greed. And so, they set out to form an event with a more altruistic purpose: Build technology, relationships, mechanisms and educational tools that better mankind. The focus at this event and the conferences that follow is to educate, expose and innovate. The focus is squarely on disruptive technology. Bitcoin and the blockchain were introduced simultaneously in a 2009 whitepaper. It’s a bit like explaining the engine and the automobile together—for the very first time. One is a technology with a myriad of applications and the potential to that drives innovation. The other is an app. Sure, it’s useful and important, but it’s just an app.

Bitcoin and the blockchain were introduced simultaneously in a 2009 whitepaper. It’s a bit like explaining the engine and the automobile together—for the very first time. One is a technology with a myriad of applications and the potential to that drives innovation. The other is an app. Sure, it’s useful and important, but it’s just an app. Likewise, 2019 is likely to be the breakout year for blockchain applications, careers, products and—perhaps most importantly—public awareness, understanding and appreciation. Just as motors and engines are not limited to automobiles, the blockchain has far more potential than serving as an engine for decentralized cash. It is too important to be just a footnote to disruptive economics. It will disrupt everything. And we are the beneficiaries.

Likewise, 2019 is likely to be the breakout year for blockchain applications, careers, products and—perhaps most importantly—public awareness, understanding and appreciation. Just as motors and engines are not limited to automobiles, the blockchain has far more potential than serving as an engine for decentralized cash. It is too important to be just a footnote to disruptive economics. It will disrupt everything. And we are the beneficiaries.

{kind=link}

{kind=link}